The dynamic development of RES is an important element of building energy independence and security of Poland and Europe. The risks associated with RES supply chains, including the risk of dependence on China, are assessed in the following analysis as significantly LOWER than the risk associated with dependence on any (especially Russian) fossil fuels. However, an active, informed, balanced and nuanced policy at a national and European level is needed for a possible overhaul of RES supply chains. The key elements of this strategy are:

The implementation of policies supporting the development of local RES supply chains should take into account the fact that today the priority is to quickly expand the capacity at the most optimal costs possible. In the Polish context, the priority is to remove barriers to the development of RES in the area of spatial planning and access to the power grid.

***

Russia’s invasion of Ukraine and the use of energy supplies as a form of weapon and mechanism of political pressure have made us painfully aware of the cost and risk of over-dependence on the fossil fuels. The response of the Western world should be not only moving away from purchase of fuels from Russia, but also fundamentally and quickly rebuilding the energy system by developing alternative energy sources to fossil fuels. A new energy system would not only guarantee geopolitical independence but would also help to reduce CO2 emissions and slow global warming.

The described scenario considers a dynamic development of RES crucial. This acceleration has become the foundation of the RePowerEU strategy announced by the European Commission, as well as the initiatives taken by the European governments. From the perspective of energy security, RES not only means independence from the availability of fuels, but also:

Despite the growing consensus on the key role of RES in the future energy mix, the pace of change and development of RES in Poland does not correspond to the seriousness of the situation. On the contrary, counter-effective actions are emerging (e.g. de facto liquidation of the prosumer PV market, new difficulties in spatial planning procedures for RES), and key changes are being implemented slowly (e.g. liberalisation of the 10H rule for onshore wind farms).

One of the doubts appearing in the discussion of the dynamic development of RES is the issue of the potential risk resulting from the dominance of China in supply chains, and thus a possible threat to their stability and resilience. In the context of the change in relations between Europe and China, in the face of Chinese support for Russia, as well as the intensifying Sino-American strategic competition, the subject of supply chain security is gaining significance. As the analysis of Circuit Breakers: Securing Europe’s Green Energy Supply Chains[1] by Agatha Kratz, Charlie Vesta and Janka Oertel of the European Council for Foreign Relations shows, the problem is recognized by European policymakers and political strategists. It also resonates in business circles, as confirmed by the recently concluded Economic Forum in Davos, where the resilience of supply chains and the management of risk of supply from China were key topics.

Are we in danger of a situation in which, as part of the development of RES, we will replace dependence on Russian fossil fuel supplies with dependence on China, as some politicians wish to interpret the issue? When looking for an answer to this question, it is worth considering three key aspects:

The European RES market currently operates to a large extent on the basis of auction systems, promoting solutions with the lowest possible costs of generating power. Thus often preferring the cheapest solutions, it allows suppliers from China to effectively enter such an open European market. Changing the current rules of the game by applying different types of preferences for local suppliers and implementing industrial policies that stimulate local supply chains is possible, but it must be selective and well-matched, so as not to cause a sharp increase in the cost of exapnding RES capacity, and consequently not to slow down the transformation.

In the PV segment, a change in the balance of power and opposing the dominance of Chinese suppliers in the field of basic, already mature silicon-based module technologies seems unlikely. The production of silicon wafers has huge advantages of scale and high energy intensity, and the production of photovoltaic modules themselves is an activity with low added value and similarly large advantage of scale. Practical attempts to build local production in this area so far have a moderate prognosis and require significant expenditures to achieve relative cost competitiveness. Currently, the premium for a local product can be up to 20-30%, which effectively prevents their mass use in large projects based on auction systems. The PV strategy should be to focus on new technologies such as perovskites, as well as innovative applications such as floating farms, agrophotovoltaics, photovoltaics with trackers, building integrated PV (BIPV), which create additional value and expand the way PV is used. In these areas, it is worth pursuing an active industrial policy within the EU and in Poland.

Great opportunities, significant also from the point of view of cybersecurity, are created by strengthening the role of European companies and diversifying supplies in the field of inverters and photovoltaic farm management systems. Looking deeper, assembly systems and the development of local competences in design, installation and operations, as well as maintenance (O&M) of photovoltaic farms, may also be an opportunity for Polish companies and engineers. Together, all these elements can allow to maintain control and maintain the stability of existing capacities, as well as ensure appropriate dynamics of development (using production capacity in China in order to accelerate the expansion of installed PV capacity).

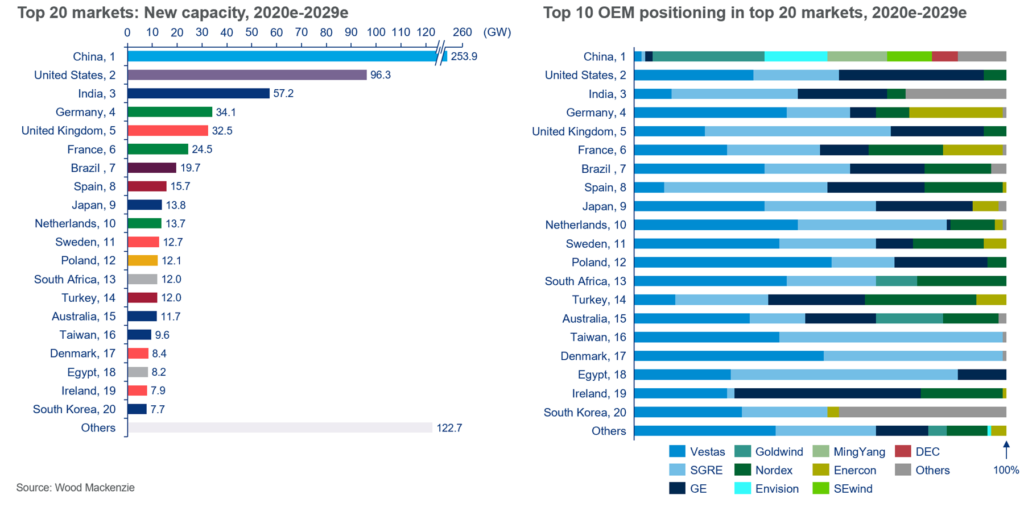

In the wind segment, European companies still have a significant market share. However, the first crucial and unfavorable for the local suppliers results of the expansion of Chinese suppliers are currently ocurring – for example the recent projects in Taranto in Italy (offshore) and the largest wind farm in Croatia, in the city of Senji (onshore).

“In April 2022, the first Italian offshore wind farm powered by turbines manufactured by the Chinese company MingYang was commissioned at the port of Taranto. This decision marked the first victory of the Chinese wind energy tycoon on the European offshore market – as stated in the report by Circuit Breakers: Securing Europe’s Green Energy Supply Chains. Just a few months earlier, the largest wind farm in Croatia, built and run by the Chinese company Norinco International, was opened in the coastal city of Senj, which was also equipped with turbines imported from China, manufactured by Shanghai Electric (one of the ten largest companies in the world in the wind sector).

European countries are increasing investment in the green transition, and projects such as Italian and Croatian wind farms are becoming a priority, not least due to the current geopolitical issues. Europe is uniting around the issue of Ukraine and striving for energy independence from Russia.

Both cases (Italian and Croatian) clearly show the challenges that the European Union must face in order for the future to be ecologically and energy-secure. In Taranto, it is a European turbine manufacturer that did not deliver the products at the required time, which in turn resulted in the entry of a Chinese competitor onto the market, while in Senj Norinco International which provides capital and equipment is not only a Chinese state-owned industrial giant, but also a defense company and a supplier of weapons and equipment for the Chinese People’s Liberation Army.”[2]

The current situation, in which five European wind turbine manufacturers are loss-making, cannot continue any longer.

The most important reason for the lack of dynamic development of local players is the slow pace of administrative procedures. If we want wind farms (offshore and onshore) to develop in Europe and Poland, while ensuring stable demand for projects, administrative processes must significantly speed up. In the wind area, there is a strong need for an appropriate auction policy that promotes local contributions in supply chains – both at European and national level. At the same time, it may be vital for the wind sector to separate the technological baskets in auctions in order to ensure adequate diversification of sources at the system level, also due to the complementarity of wind and solar sources from the point of view of system stability.

Supply chains of battery and hydrogen technologies crucial for the development of the RES market are just being formed. This is an important moment and time to implement an active industrial and trade policy, which should lead to independence from fossil fuels. It is necessary to build local and European competences and scale, as well as strategic partnerships both in the transatlantic dimension and with the countries of the Middle East or Africa which have ideal conditions e.g. for the production of hydrogen on the basis of electrolysis based on solar sources. New technologies are also an area of rapidly growing strategic competition with China, and from the perspective of practical market observers, Europe is already starting to lag behind, as can be seen for example by the better cost position of Chinese suppliers in regards to batteries.

A strategy at the European level that takes into account the stability of the RES supply chain must take into account two more important elements:

From the perspective of the further evolution of the RES market, it seems crucial to have a conscious, balanced and nuanced policy at the national and European level, which will ensure the fastest possible development of RES capacity, while optimizing costs and managing strategic risk. The key elements of this strategy are:

Given the scale of the necessary implementation of renewables in all technologies and entire Europe, the optimisation of supply chains should not slow down or overshadow the transformation. Regulators should be focused on creating conditions to accelerate the development of RES. Particularly in the field of administrative and location decisions, the development of energy networks for smooth cooperation with RES, as well as the modification of energy market rules to facilitate the use of RES in the system. Progress

in these areas, especially in Poland, may unleash the potential of RES, which will quickly have a positive impact on energy security, and at the same time may become a flywheel of the Polish economy.

Article publication date: 28 June 2022

Łukasz Dobrowolski, MBA, Director of Climate Strategies and Energy Market

Climate and Strategy Foundation

Director of Energy Strategies, Climate Strategies Poland Foundation. At the Foundation, he is responsible for projects of strategies for reducing carbon footprint emissions and deals with issues related to the energy market and energy transformation of enterprises. As a consultant and partner at McKinsey & Company, he advised the largest Polish and global corporations on strategy and business development. He managed large business organizations, among others as a Managing Director at Polkomtel S.A. For over 10 years, he has been an active investor and entrepreneur involved in the renewable energy sector, in the business segment, local governments and individual clients. Advisor, manager and entrepreneur.

*****

This study is based on the conclusions of the discussion on the role of renewable energy sources in the energy security of Poland and Europe. The discussion was attended by:

The above conclusions reflect the situation of the Polish and European economy based on current knowledge at the time of publication of the document and are merely the conclusions of the author, and as such do not fully reflect the views of the participants of the aforementioned discussion.

[1]https://ecfr.eu/wp-content/uploads/2022/05/Circuit-breakers-Securing-Europes-green-energy-supply-chains_Kratz_Oertel_Vest.pdf

[2] https://ecfr.eu/wp-content/uploads/2022/05/Circuit-breakers-Securing-Europes-green-energy-supply-chains_Kratz_Oertel_Vest.pdf